Financial Clarity Is Not a Feeling. It’s a System.

- Sam Sur

- Dec 22, 2025

- 12 min read

Why confidence fades under pressure, and how real clarity is engineered

Most people who seem financially successful feel clear about their money: Income is steady. Accounts are growing. Nothing feels urgent. When asked how things are going, the answer is usually some version of “pretty good.”

But that feeling is not clarity. It’s comfort.

Clarity truly shows itself when something in your life changes: a health issue, a business slowdown, a market pullback, a family transition, or a sudden need for cash. In those moments, people discover that their finances were never really designed to handle disruption. They were simply built piece by piece over time.

Financial clarity is not reassurance, or optimism; and it certainly isn’t a set of projections that assume life will behave.

Clarity is what remains when conditions change. Stability comes from design.

This matters because financial decisions made without clarity tend to hold up only when life behaves, and life rarely does.

The Illusion of Financial Clarity

In stable periods, clarity feels automatic. Income arrives. Bills are paid. Portfolios appear diversified. Advisors provide reassurance. Plans exist—often detailed, polished, and confidently projected.

Yet this sense of clarity is fragile because it rests on unexamined assumptions:

Income will continue uninterrupted

Health will remain stable

Markets will recover on schedule

Capital will always be accessible

Decision-makers will always be present and capable

History shows otherwise. Federal Reserve data consistently shows that even well-earning households often face liquidity stress when income or markets shift. Net worth can look strong on paper while usable capital is limited when it is needed most.

The issue is not a lack of intelligence or effort.The issue is that most financial lives are never designed as integrated systems.

✨ Data Insight:

Many Households Lack Financial Flexibility.

According to the Federal Reserve, nearly 4 in 10 U.S. households would struggle to cover a $400 emergency expense without borrowing or selling something, even if they appear financially stable on paper. That gap isn’t ignorance — it’s a planning blind spot.

When Finances Aren’t Built Without a System

When finances don’t have a coherent structure, stress shows up slowly but persistently. A business owner may realize too much depends on their day-to-day involvement. A family may discover most of its wealth is tied up and inaccessible when needed. An illness may force rushed decisions. A market downturn may trigger selling at exactly the wrong time. Over time, common weaknesses emerge:

Too much depends on one source

Too many assets can’t move easily

Protection doesn’t match true needs

Decisions get made under stress

Personal, business, and family goals conflict

These are not planning mistakes - they are architecture failures.

✨ Insight:

Overlooked Risks Often Cause Setbacks

Industry research shows many financial setbacks are not caused by market downturns alone, but by overlooked risks like reliance on a single income or missing protection coverage. Lack of coordination between plans is a bigger threat than volatility itself.

Why Most Plans Don’t Hold Up

Most financial plans are built like snapshots: they reflect a moment in time, a set of assumptions, and a straight line into the future. As long as life behaves that way, everything seems fine.

But life doesn’t - careers change, families evolve, health shifts. and markets swing. Plans that don’t adapt often collapse quietly before people realize they’re at risk.

✨ Insight:

Plans Abandoned After Life Events

Research from professional planning organizations consistently shows that financial plans are most often ignored after major life events, not because they were poorly made, but because they weren’t designed to evolve as circumstances did.

Clarity arises from preparing for change, not predicting it.

✨ Insight:

Systems Beat Ad-Hoc Decisions

Research increasingly shows that people who operate within a structured financial planning process experience measurably better outcomes than those relying on informal or reactive decision-making.

Initial findings from the CFP Board’s Financial Planning Longitudinal Study indicate that households working with professional planners are more likely to maintain emergency reserves, regularly review their financial decisions, and report feeling financially stable over time. These outcomes are tied less to market conditions and more to disciplined planning behaviors built into a system.¹

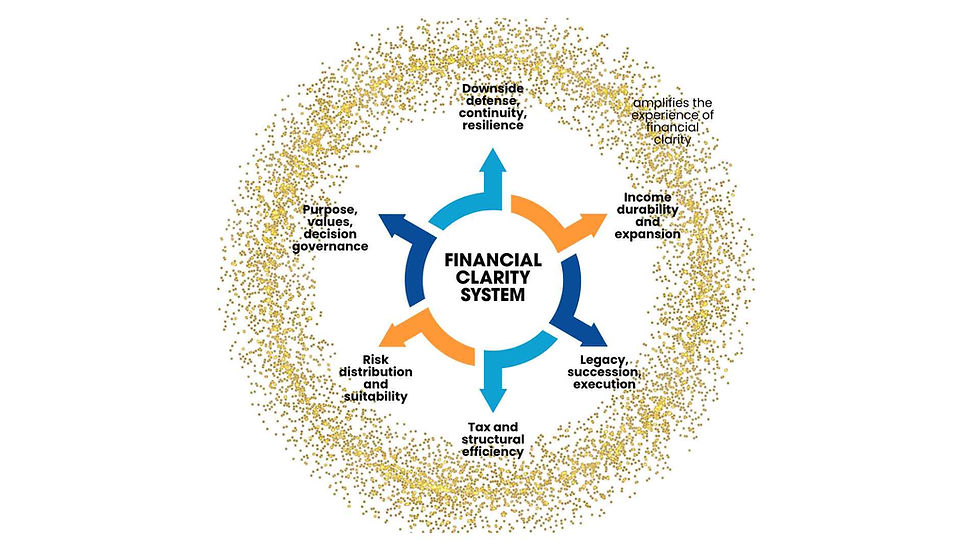

What Is a “Financial Clarity System”?

A financial clarity system is a structured approach to understanding how income, assets, risks, and decisions interact under changing conditions. It identifies hidden dependencies, establishes priorities, and defines decision rules before stress or disruption occurs. The purpose of a financial clarity system is not to predict outcomes, but to ensure confident, coordinated decisions when life, markets, or circumstances change.

A clarity-delivering system has four defining characteristics:

It reveals hidden fragility

It forces prioritization (not optimization)

It creates decision rules before stress

It stays alive over time

Anything that doesn’t do all four is not a clarity system — it’s documentation.

What a Financial Clarity System Is Not

A Financial Clarity System is not built around product presentation, portfolio review, or replacement for ongoing financial planning. It does not focus on performance projections, specific investments, or implementation decisions. Its purpose is to create understanding and structure before any recommendations are considered.

What Clarity-driven Financial Lives Have in Common

When you look at people who stay steady through change, a pattern emerges: they don’t start by chasing returns or optimizing details. They start by making sure the basics won’t collapse under pressure. Then they build outward, one priority at a time, in a deliberate order.

Clear financial lives tend to share a common trait. They weren’t built around growth first. They were built around stability.

✨ Insight:

Structure Improves Financial Behavior

Studies comparing advised versus non-advised households show that individuals who follow a structured financial planning process are significantly more likely to engage in foundational behaviors, such as maintaining liquidity, planning for taxes, preparing estate documents, and managing risk exposure.

In multiple surveys, clients of professional planners were 8–32% more likely to have emergency funds, wills, insurance coverage aligned to their needs, and coordinated long-term plans than those without a formal planning system.²

Those priorities tend to show up consistently:

Protection Architecture

First, they make sure life won’t fall apart if something goes wrong. This isn’t doom-saying. It’s continuity planning. They consider: what happens if income stops? If health changes? If someone crucial is no longer available? They reinforce weaknesses before disruption forces them.

✨ Insight:

Protection Gaps Are Common and Costly

Multiple industry studies find that most protection gaps are uncovered only after a triggering event such as disability, illness, or death — meaning people often assume they’re covered when they’re not.

👉 Thinking about this early preserves options. Ignoring it often forces trade-offs later.

Income Durability

Next, they look at how dependable their income really is - not just how much they earn this year, but how brittle that income might be.

They ask: is income tied to their time? Their health? One role or business? What happens if that changes?

✨ Insight:

Income Shocks Have Lingering Effects

Studies show that more than 60% of households that experience a major income disruption face lasting financial effects for three years or more, even if income later recovers. This isn’t rare — it’s common.

👉 Durable income makes everything else easier. Fragile income makes everything harder.

Tax Efficiency Over Time

Taxes don’t feel dramatic, but they influence results every year. People with clarity think beyond this year’s bill. They consider how income and assets are taxed now versus later and how timing decisions affect outcomes long term.

✨ Insight:

Tax Inefficiency Drains Long-Term Wealth

Long-term studies show that tax inefficiency can reduce lifetime wealth more than market downturns, especially for high earners and business owners. Small choices today can have outsized consequences decades later.

👉 Small choices today can have outsized consequences decades later.

Risk Exposure Alignment

Risk isn’t something you avoid. It’s something you measure. Clear thinkers distinguish between risks that are acceptable, painful, or devastating. They understand how different parts of their financial life behave when stress arrives.

✨ Insight:

Misunderstood Risk Leads to Poor Outcomes

During major market declines, investors who don’t have a clear understanding of their risk exposure are far more likely to sell at the bottom, turning temporary volatility into permanent losses.

👉 Knowing risk doesn’t eliminate volatility — it prevents panic.

Growth with Intent

Growth matters, but it works best when it’s grounded in stability. Focus on how growth interacts with income, taxes, liquidity, and risk. When growth is aligned with the rest of the picture, it becomes a tool, not a source of stress.

✨ Insight:

Behavioral Decisions Damage Returns

Market data shows the largest drag on long-term returns often comes not from downturns themselves, but from poor decisions made during downturns — reacting instead of adapting.

👉 Well-aligned growth strategies feel uneventful until conditions turn.

Legacy and Decision Continuity

Finally, clarity extends beyond the individual. It means thinking about who can act if someone is unavailable, how decisions are made under pressure, and whether intentions can actually be executed.

✨ Insight:

Most Estate Plans Don’t Work as Expected

Research indicates many estate plans fail not because they don’t exist, but because they are outdated, underfunded, or disconnected from how assets are actually held — especially for business owners planning transition.

👉 Plans that only work when one person is present are fragile by definition.

Clarity Is Lived, Not Managed

When these priorities are addressed in the right order, something changes: money becomes quieter. Decisions feel less urgent. Life feels less cluttered by financial loose ends. Complexity still exists, but it’s coordinated rather than chaotic.

For people with demanding lives and growing responsibilities, this is often the biggest shift. Not more control, but less noise.

✨ Data Insight:

Systems Reduce Stress, Not Just Risk

Financial systems don’t only improve balance sheets; they reduce emotional strain.

Research tied to the CFP Board’s longitudinal work shows that households operating within a structured planning relationship report lower financial anxiety, fewer family conflicts related to money, and higher confidence during periods of uncertainty, even when external conditions deteriorate.³

In other words, systems don’t remove volatility—but they change how people experience it.

Why the Order Makes the Difference

Many people start with growth and work backward. Starting with growth can feel logical when everything is working. But without stability underneath, growth adds pressure to parts of the system that were never designed to carry it. The result is progress that looks strong until conditions change. Order may feel less impactful in good times, but it often leads to uncomfortable compromises when conditions change. When stability comes first, confidence is built into the structure underneath.

Why Financial Systems Work

Financial outcomes are rarely determined by one decision.They are shaped by patterns of behavior over time.

Research across financial planning, behavioral economics, and household finance consistently shows that people who operate within a structured planning system:

Maintain higher levels of emergency liquidity

Make fewer panic-driven decisions during market stress

Coordinate taxes, risk, and investments more effectively

Update plans more consistently as life changes

Report higher long-term financial confidence

Importantly, these benefits show up even when markets are volatile or income is disrupted. The advantage comes from structure, not prediction.

Financial systems don’t guarantee better markets.They produce better decisions when markets - and life - don’t cooperate.

How to Build a Financial Clarity System (Step-by-Step)

A decision system for life under uncertainty

A financial clarity system is built through a repeatable process that prepares households to make decisions before pressure arrives. Here are the steps to build robust financial clarity.

1. Surface Reality (Before Solutions)

Clarity begins by removing assumptions.

This step removes assumptions by revealing how income, access, and responsibilities actually function today. Before recommendations, projections, or products, the system must surface:

Where income comes from

What breaks if income stops

What cannot be accessed quickly

What depends on one person

What decisions are currently undefined

This step is diagnostic, not advisory. So if someone leaves this phase feeling “good” instead of slightly uncomfortable, the system has failed.

Outcome:

A shared, unfiltered view of reality — including blind spots.

2. Map Financial Dependencies

Assets matter less than what depends on them.

This step shows what truly depends on what, so pressure points are visible before stress exposes them. Most people organize finances by accounts and balances.Clarity systems organize by dependencies. The system must explicitly map:

Income → lifestyle → obligations

Health → earning capacity → liquidity

Business roles → cash flow → family needs

Market exposure → timing risk → decision pressure

This is where people realize: “I didn’t know how much depended on that.”

Outcome:

Understanding where pressure concentrates when conditions change.

3. Set the Order of Priorities

Stability first. Growth second.

This step establishes what must not fail first, ensuring stability comes before flexibility and growth. Clarity collapses when everything is treated as equally important. The system must force sequencing, typically:

What must not fail

What must continue

What can flex

What can grow

This is where Protect-first logic lives, without naming it. Most people skip this and jump straight to growth.That’s why clarity disappears under stress.

Outcome:

Agreement on what comes first — and what can wait.

4. Define Decision Boundaries (The definition of "Enough")

Boundaries reduce emotional decisions.

Clarity requires boundaries. This step clarifies what “enough” looks like, reducing emotional decisions and constant second-guessing. The system must answer:

How much income is enough?

How much liquidity is enough?

How much risk is acceptable?

What capital is truly excess?

Without these definitions, every decision feels urgent and emotional. This step removes the constant question of “should we do more?”

Outcome:

Clear thresholds that reduce decision fatigue.

5. Create Decision Rules Before Stress

Calm decisions beat reactive ones.

This step defines how decisions will be made when conditions change, so that reactions are replaced with prepared responses. Clarity is sustained by decisions made before pressure arrives. The system must lay out:

What happens if income drops by X%

What happens if markets fall by Y%

What triggers reallocation or restraint

Who decides if someone is unavailable

This is governance, not forecasting. Most people wait to decide until stress forces their hand — and then regret it.

Outcome:

Confidence during disruption because decisions are already framed.

6. Align the Pieces

Structures now have reasons.

This step ensures protection, liquidity, risk, and growth are coordinated around real priorities rather than isolated choices. Structures, aka, insurance policies, investment portfolios, trusts and estate documents, etc., must be discussed only after clarity exists. At this stage, the system aligns:

Protection to real dependencies

Liquidity to actual access needs

Risk to defined tolerances

Growth to excess capital

Tax decisions to lifetime impact

The difference is that now every structure has a reason.

Outcome:

Fewer, cleaner decisions that feel obvious instead of complex.

7. Review with Intent

Clarity fades without rhythm.

Clarity is not a one-time event. This step keeps clarity current by revisiting decisions as life, income, and responsibilities evolve. The system must intentionally revisit:

Life changes

Income changes

Business changes

Family changes

Market changes

Most clarity erodes because reviews are reactive or skipped entirely.

Outcome:

Clarity stays current without becoming burdensome.

Financial Clarity - Key Takeaways

What becomes clear when everything is viewed together.

Financial clarity comes from how things are set up, not how they feel. Most financial stress doesn’t come from markets. It comes from not seeing what depends on what. Plans tend to break because they assume life will stay stable instead of preparing for change.Real clarity puts protection, dependable income, access to cash, and decision rules in place before focusing on growth. When clarity is in place, people make calmer decisions, avoid second-guessing, and face fewer forced trade-offs.

The key takeaways from a Financial Clarity System focus on understanding where risk truly exists, how decisions connect across your financial life, and what deserves attention first.

Financial clarity is structural, not emotional.

Most financial stress comes from hidden dependencies, not market volatility.

Plans fail because they assume stability instead of designing for change.

A financial clarity system prioritizes protection, income durability, liquidity, and decision rules before growth.

Clarity improves outcomes by reducing panic, decision fatigue, and forced trade-offs.

What Changes After a Financial Clarity Session

After the session, families and business owners usually:

Know which risks need attention now and which can safely wait

See how personal, business, and financial decisions affect each other

Feel more confident making choices because priorities and boundaries are clear

When a Financial Clarity Session Is Most Useful

A Financial Clarity Session is most helpful during times of change — when income is rising, a business is growing, family responsibilities are shifting, or retirement is getting closer. It’s often used when things seem mostly fine, but questions are starting to linger. Getting clarity early keeps options open and reduces the need to make rushed decisions later.

A Final Thought

Most people don’t fail financially. They drift. Things work well enough for long enough that deeper questions get postponed. Then life forces decisions before the structure is ready.

Financial clarity isn’t something you suddenly feel.It’s something you build intentionally, often through a structured clarity conversation. And its real value shows up when not everything is going well.

Schedule a Clarity Session if you want to find out about the Palatino Approach

Or, Download the Clarity Checklist to see where you stand.

Footnotes & Sources

CFP Board, Financial Planning Longitudinal Study (Initial Findings).

Early results indicate that households working with CERTIFIED FINANCIAL PLANNER® professionals are more likely to maintain emergency funds, engage in ongoing planning behaviors, and report living comfortably compared to households without structured planning relationships.

CFP Board, Financial Planning Association (FPA), and Investment Funds Institute of America (IFA), comparative client outcome studies.

Research shows that individuals with professional financial planning support are 8–32% more likely to exhibit key planning behaviors, including emergency savings, insurance alignment, retirement planning, and estate preparation.

CFP Board, Client Well-Being and Financial Confidence Research.

Findings suggest that structured financial planning correlates with lower financial stress, reduced family conflict over money, and greater confidence during economic uncertainty, independent of market performance.

Federal Reserve Board, Report on the Economic Well-Being of U.S. Households.

The Fed consistently reports that approximately 37–40% of U.S. adults would struggle to cover a $400 emergency expense, underscoring the gap between perceived financial health and real liquidity.

Morningstar, Dalbar, Vanguard, investor behavior research.

Long-term studies show that behavioral responses during volatility—not market declines themselves—are the primary drivers of investor underperformance, reinforcing the importance of decision structure.

Tax Policy Center & academic retirement-income research.

Research demonstrates that tax inefficiency over a lifetime can erode total wealth as much as or more than market downturns, particularly for high-income earners and business owners.

American College of Trust and Estate Counsel (ACTEC) and estate administration studies.

Studies indicate that many estate plans fail in execution due to outdated documents, misaligned ownership structures, or lack of decision continuity.

Comments